Everyone Has the Same Script

Everyone Has the Same Script

FOMO until year end on strong seasonals only to collapse in 2023. In essence, the Morgan Stanley “tactical call” for a rally to 4200 and then drop to 3200 next year. Easy, right? It’s the nobody is long argument by the brokerage houses and that the pain trade is up. Yet, you saw on Friday at 9:25AM, Nasdaq futures were up a full percent before the open, followed by a drop to flat by 10 AM and then at lunch time hovering down almost a percent. Sure, Friday was a big options expiration day, but if the market truly had this FOMO element in force, one would think up moves would get bought not sold. Even a typically “easy” trading move ripping all software stocks, especially security, on the $PANW strong quarter and outlook couldn’t keep $CRWD, up 5% pre market, from going down on the day. It is true, in my entire career, I would guestimate 80% plus of the time stock seasonals cause a massive rally November through January regardless of fundamentals. Yes, it is seasonals, buybacks before calendar year end, light issuance calendar and lastly, the desire for hedge funds to collect as much performance fees as possible.

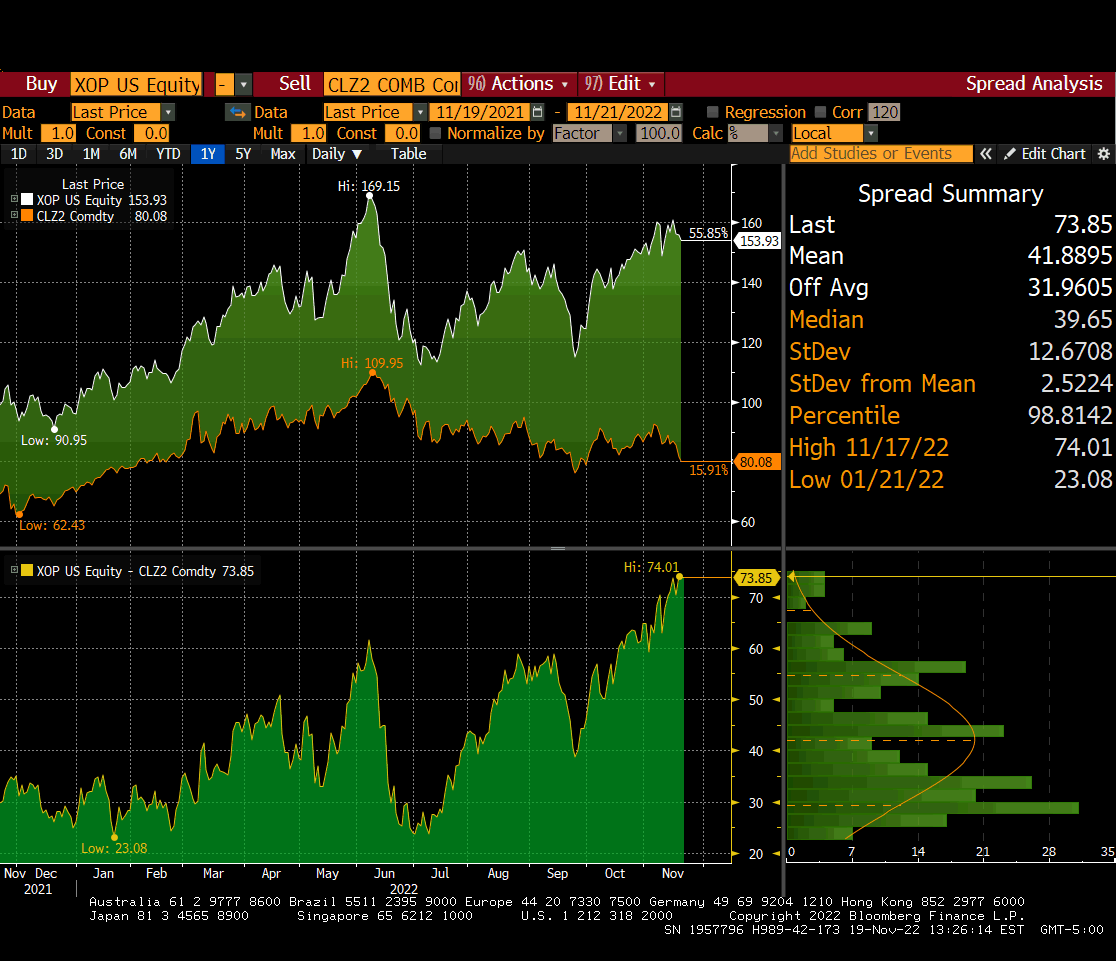

What is very different this year is the massive performance discrepancies between strategies. Equity long-short has most all managers down double digits, barring the more levered market neutral type of styles. Dedicated funds such as technology and energy are generally moving the opposite direction with tech specialists down huge and energy mostly all bullish and strongly positive. You can actually see the long energy trade fighting for its life lately with the commodities coming in hard but the stocks hanging relatively tough. The chart below shows the historical spread of oil to $XOP which is now at its widest in 2 years. I completely understand the bull case of under investment and the stocks are “cheap” on the strip, but I would be looking for funds to lock in profits in this sector as they already caught a great non correlated move to the overall markets in 2022. Said differently, does getting longer energy stocks help those funds incrementally from here? No. The same way technology funds under massive water have no shot at earning performance fees in 2022 and are likely to have size redemptions for January 1, 2023. CTA’s are having a banner year but hit a snafu being short for the 7% up move 11/10-11. Their models had them turn buyer likely through year end if the market stays here or higher to the tune of $25 billion per week. Mutual fund inflows also turned positive to the same dollar amount roughly per month. Buybacks are happening as we are out of the blackout period as well. Yet, despite all of this, last week being a down week should be somewhat disappointing to the bull case.

Perhaps then its “don’t fight the Fed” working in real time? Not the narrative but they are selling $95 billion of securities per month to reduce their balance sheet. When they sell such securities, someone is buying them (a bank, investors, sovereigns etc) which reduces capital available to purchase other securities, at the margin. Similarly, money supply has turned negative. David Rosenberg, a well-known market strategist, is convinced the money supply turning negative means we are heading into a recession and that inflation is about to drop like a rock. When you read this a second time, you should ask yourself am I really buying stocks because inflation will come in hard (the common bull narrative), allowing the Fed to take their foot off the breaks? But, in a recession, aren’t profits (EPS) going to come in hard and with 2023 bearish projections of $200 EPS for the S&P 500, the market is pretty richly valued at 4000 (20x) by any historical metrics especially with higher rates? Plus, check out the Atlanta Fed GDP Now forecast which is currently showing 4.2% growth in the 4Q at this point in the quarter. One can argue this gives the Fed cover to keep going, stay high and “we ain’t seen nothing yet” on the slowdown and pain in the economy. If this is what a 4% growth quarter feels like (tons of EPS revisions lower), then what will negative growth feel like from here?

So, what is our suggestion or script for substack readers?