The Bon Jovi market

The free look ahead on 1Q earnings

It’s a Bon Jovi Market – and we are half way there

“Woah, we’re half way there

Woah, livin on a prayer

Take my hand, we’ll make it I swear

Woah, livin on a prayer.”

Ok, fine it’s a bit cheesy, but we think apropos for this market. We think we have ½ the formula for a true market bottom. The dynamics of pain (losses) and discounting news in the markets requires 1) acceptance, 2) time, 3) sentiment and 4) reset expectations. We have resolved #1 and #3, while #2 and #4 are days/weeks away. Let’s discuss.

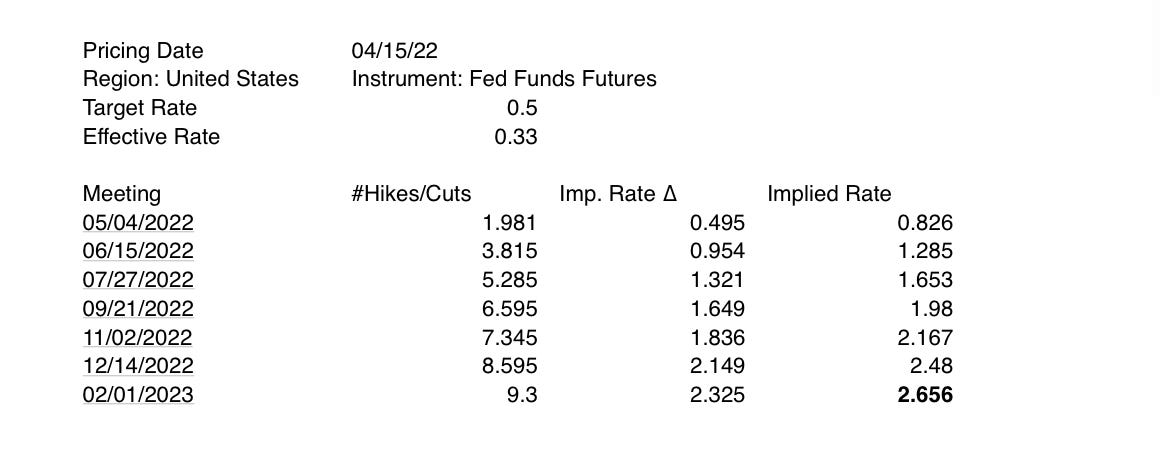

At a recent dinner with friends who are in the bond market we sensed despondency. They said clients were not selling what they had, planning to hold til maturity, but they were not adding either. Volumes were anemic and everyone was waiting for stabilization to buy. Since the bond market is having its worst annual start since 1973, you can see why such reticence exists, albeit isn’t that when you are supposed to buy, when no one else wants to do so? Typically yes! We are certainly at peak hawkish Fed with two 50 bps hikes all but guaranteed the next two meetings and Fed fund implying 8 more total hikes the rest of 2022 and 2.65% for the 10 year by February of next year. In our minds, this is the NEUTRAL rate and the Fed is going there regardless of the data points ahead. Does anyone really think the Fed should still be stimulating? Hell no. So the market is quickly discounting where the Fed is taking us already while most agree that inflation looks like it might have peaked with the March reports. Can this change for the worse and expect more hikes past neutral? Unlikely in our view.

So, the acceptance that the Fed is tightening conditions quickly to get to neutral seems to finally be widely understood. From a time perspective, 2022 has given us basically 4 months of pain with occasional relief for those facing acceptance to lighten up. After all, $TLT had a couple of rally tries along the way, albeit not as extreme as the stock market where the $QQQ bounced 15% over a two-week period starting mid-March. The $QQQ has dropped 9% since that move, given back ½ that bounce and is now down 15% for 2022. Remind yourself for a second how tech heavy both the $SPY and $QQQ are. 25% of the $SPY is Apple, Microsoft, Amazon, Tesla, Google, Nvidia and Meta. The $QQQ is almost 50% made up of those same stocks. The market or indices cannot go anywhere without tech stocks. Is January thru April enough time to discount higher rates and economic slowing? Perhaps, but not if expectations still remain too high.